Consumer Math

We have to work with money every day. While balancing your checkbook or calculating your monthly expenditures on espresso requires only arithmetic, when we start saving, planning for retirement, or need a loan, we need more mathematics.

Simple Interest

Discussing interest starts with the principal, or amount your account starts with. This could be a starting investment, or the starting amount of a loan. Interest, in its most simple form, is calculated as a percent of the principal. For example, if you borrowed $100 from a friend and agree to repay it with 5% interest, then the amount of interest you would pay would just be 5% of 100: $100(0.05) = $5. The total amount you would repay would be $105, the original principal plus the interest.

Simple One-Time Interest

[latex-display]I=P_0{r}\\[/latex-display]

[latex-display]A=P_0+I=P_0+P_0{r}=P_0(1+r)\\[/latex-display]

- I is the interest

- A is the end amount: principal plus interest

- P0 is the principal (starting amount)

- r is the interest rate (in decimal form. Example: 5% = 0.05)

Example 1

A friend asks to borrow $300 and agrees to repay it in 30 days with 3% interest. How much interest will you earn?

Solution

| P0 = $300 |

the principal |

| r = 0.03 |

3% rate |

| I = $300(0.03) = $9 |

You will earn $9 interest. |

One-time simple interest is only common for extremely short-term loans. For longer term loans, it is common for interest to be paid on a daily, monthly, quarterly, or annual basis. In that case, interest would be earned regularly. For example, bonds are essentially a loan made to the bond issuer (a company or government) by you, the bond holder. In return for the loan, the issuer agrees to pay interest, often annually. Bonds have a maturity date, at which time the issuer pays back the original bond value.

Example 2

Suppose your city is building a new park, and issues bonds to raise the money to build it. You obtain a $1,000 bond that pays 5% interest annually that matures in 5 years. How much interest will you earn?

Solution

Each year, you would earn 5% interest: $1000(0.05) = $50 in interest. So over the course of five years, you would earn a total of $250 in interest. When the bond matures, you would receive back the $1,000 you originally paid, leaving you with a total of $1,250.

We can generalize this idea of simple interest over time.

Simple Interest over Time

[latex-display]I=P_0{rt}\\[/latex-display]

[latex-display]A=P_0+I=P_0+P_0{rt}=P_0(1+rt)\\[/latex-display]

- I is the interest

- A is the end amount: principal plus interest

- P0 is the principal (starting amount)

- r is the interest rate in decimal form

- t is time

The units of measurement (years, months, etc.) for the time should match the time period for the interest rate.

APR—Annual Percentage Rate

Interest rates are usually given as an annual percentage rate (APR)—the total interest that will be paid in the year. If the interest is paid in smaller time increments, the APR will be divided up.

For example, a 6% APR paid monthly would be divided into twelve 0.5% payments.

A 4% annual rate paid quarterly would be divided into four 1% payments.

Example 3

Treasury Notes (T-notes) are bonds issued by the federal government to cover its expenses. Suppose you obtain a $1,000 T-note with a 4% annual rate, paid semi-annually, with a maturity in 4 years. How much interest will you earn?

Solution

Since interest is being paid semi-annually (twice a year), the 4% interest will be divided into two 2% payments.

| P0 = $1000 |

the principal |

| r = 0.02 |

2% rate per half-year |

| t = 8 |

4 years = 8 half-years |

| I = $1000(0.02)(8) = $160 |

You will earn $160 interest total over the four years. |

Try It Now

A loan company charges $30 interest for a one month loan of $500. Find the annual interest rate they are charging.

Compound Interest

With simple interest, we were assuming that we pocketed the interest when we received it. In a standard bank account, any interest we earn is automatically added to our balance, and we earn interest on that interest in future years. This reinvestment of interest is called compounding.

Suppose that we deposit $1000 in a bank account offering 3% interest, compounded monthly. How will our money grow?

The 3% interest is an annual percentage rate (APR)—the total interest to be paid during the year. Since interest is being paid monthly, each month, we will earn [latex]\displaystyle\frac{3\%}{12}\\[/latex] = 0.25% per month.

In the first month,

P0 = $1000

r = 0.0025 (0.25%)

I = $1000 (0.0025) = $2.50

A = $1000 + $2.50 = $1002.50

In the first month, we will earn $2.50 in interest, raising our account balance to $1002.50.

In the second month,

P0 = $1002.50

I = $1002.50 (0.0025) = $2.51 (rounded)

A = $1002.50 + $2.51 = $1005.01

Notice that in the second month we earned more interest than we did in the first month. This is because we earned interest not only on the original $1000 we deposited, but we also earned interest on the $2.50 of interest we earned the first month. This is the key advantage that compounding of interest gives us.

Calculating out a few more months:

| Month |

Starting balance |

Interest earned |

Ending Balance |

| 1 |

1000.00 |

2.50 |

1002.50 |

| 2 |

1002.50 |

2.51 |

1005.01 |

| 3 |

1005.01 |

2.51 |

1007.52 |

| 4 |

1007.52 |

2.52 |

1010.04 |

| 5 |

1010.04 |

2.53 |

1012.57 |

| 6 |

1012.57 |

2.53 |

1015.10 |

| 7 |

1015.10 |

2.54 |

1017.64 |

| 8 |

1017.64 |

2.54 |

1020.18 |

| 9 |

1020.18 |

2.55 |

1022.73 |

| 10 |

1022.73 |

2.56 |

1025.29 |

| 11 |

1025.29 |

2.56 |

1027.85 |

| 12 |

1027.85 |

2.57 |

1030.42 |

To find an equation to represent this, if Pm represents the amount of money after m months, then we could write the recursive equation:

P0 = $1000

Pm = (1 + 0.0025)Pm–1

You probably recognize this as the recursive form of exponential growth. If not, we could go through the steps to build an explicit equation for the growth:

P0 = $1000

P1 = 1.0025P0 = 1.0025 (1000)

P2 = 1.0025P1 = 1.0025 (1.0025 (1000)) = 1.00252(1000)

P3 = 1.0025P2 = 1.0025 (1.00252(1000)) = 1.00253(1000)

P4 = 1.0025P3 = 1.0025 (1.00253(1000)) = 1.00254(1000)

Observing a pattern, we could conclude

Pm = (1.0025)m($1000)

Notice that the $1000 in the equation was P0, the starting amount. We found 1.0025 by adding one to the growth rate divided by 12, since we were compounding 12 times per year. Generalizing our result, we could write

[latex-display]\displaystyle{P_m}=P_0\left({1}+\frac{r}{k}\right)^m\\[/latex-display]

In this formula:

m is the number of compounding periods (months in our example)

r is the annual interest rate

k is the number of compounds per year.

While this formula works fine, it is more common to use a formula that involves the number of years, rather than the number of compounding periods. If N is the number of years, then m = Nk. Making this change gives us the standard formula for compound interest.

Compound Interest

[latex-display]\displaystyle{P_N}=P_0\left({1}+\frac{r}{k}\right)^Nk\\[/latex-display]

- PN is the balance in the account after N years.

- P0 is the starting balance of the account (also called initial deposit, or principal)

- r is the annual interest rate in decimal form

- k is the number of compounding periods in one year.

If the compounding is done annually (once a year), k = 1.

If the compounding is done quarterly, k = 4.

If the compounding is done monthly, k = 12.

If the compounding is done daily, k = 365.

The most important thing to remember about using this formula is that it assumes that we put money in the account once and let it sit there earning interest.

Example 4

A certificate of deposit (CD) is a savings instrument that many banks offer. It usually gives a higher interest rate, but you cannot access your investment for a specified length of time. Suppose you deposit $3000 in a CD paying 6% interest, compounded monthly. How much will you have in the account after 20 years?

Solution

In this example,

| P0 = $3000 |

the initial deposit |

| r = 0.06 |

6% annual rate |

| k = 12 |

12 months in 1 year |

| N = 20 |

since we’re looking for how much we’ll have after 20 years |

So [latex]\displaystyle{P}_20=3000\left(1+\frac{0.06}{12}\right)^{20\cdot{12}}=\$9930.61\\[/latex] (round your answer to the nearest penny)

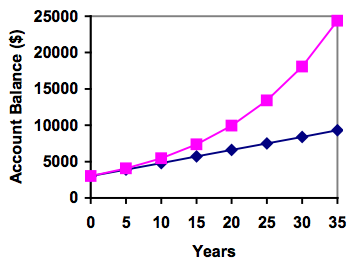

Let us compare the amount of money earned from compounding against the amount you would earn from simple interest

| Years |

Simple Interest ($15 per month) |

6% compounded monthly = 0.5% each month. |

| 5 |

$3900 |

$4046.55 |

| 10 |

$4800 |

$5458.19 |

| 15 |

$5700 |

$7362.28 |

| 20 |

$6600 |

$9930.61 |

| 25 |

$7500 |

$13394.91 |

| 30 |

$8400 |

$18067.73 |

| 35 |

$9300 |

$24370.65 |

As you can see, over a long period of time, compounding makes a large difference in the account balance. You may recognize this as the difference between linear growth and exponential growth.

As you can see, over a long period of time, compounding makes a large difference in the account balance. You may recognize this as the difference between linear growth and exponential growth.

Evaluating Exponents on the Calculator

When we need to calculate something like 53 it is easy enough to just multiply 5 ⋅ 5 ⋅ 5 = 125. But when we need to calculate something like 1.005240, it would be very tedious to calculate this by multiplying 1.005 by itself 240 times! So to make things easier, we can harness the power of our scientific calculators.

Most scientific calculators have a button for exponents. It is typically either labeled like:

^, yx, or xy.

To evaluate 1.005240 we'd type 1.005 ^ 240, or 1.005 yx 240. Try it out—you should get something around 3.3102044758.

Example 5

You know that you will need $40,000 for your child’s education in 18 years. If your account earns 4% compounded quarterly, how much would you need to deposit now to reach your goal?

Solution

In this example,

We’re looking for

P0.

| r = 0.04 |

4% |

| k = 4 |

4 quarters in 1 year |

| N = 18 |

Since we know the balance in 18 years |

| P18 = $40,000 |

The amount we have in 18 years. |

In this case, we’re going to have to set up the equation, and solve for

P0.

[latex-display]\displaystyle{40000}=P_0\left(1+\frac{0.04}{4}\right)^{18\cdot{4}}\\[/latex-display]

[latex-display]\displaystyle{40000}=P_0(2.0471)\\[/latex-display]

[latex-display]\displaystyle{P}_0=\frac{40000}{2.0471}=\$19539.84\\[/latex-display]

So you would need to deposit $19,539.84 now to have $40,000 in 18 years.

Rounding

It is important to be very careful about rounding when calculating things with exponents. In general, you want to keep as many decimals during calculations as you can. Be sure to keep at least 3 significant digits (numbers after any leading zeros). Rounding 0.00012345 to 0.000123 will usually give you a “close enough” answer, but keeping more digits is always better.

Example 6

To see why not over-rounding is so important, suppose you were investing $1000 at 5% interest compounded monthly for 30 years.

| P0 = $1000 |

the initial deposit |

| r = 0.05 |

5% |

| k = 12 |

12 months in 1 year |

| N = 30 |

since we’re looking for the amount after 30 years |

Solution

If we first compute [latex]\displaystyle\frac{r}{k}\\[/latex], we find [latex]\displaystyle\frac{0.05}{12}=0.00416666666667\\[/latex].

Here is the effect of rounding this to different values:

| [latex]\displaystyle\frac{r}{k}\\[/latex] rounded to |

Gives P30 to be |

Error |

|---|

| 0.004 |

$4208.59 |

$259.15 |

| 0.0042 |

$4521.45 |

$53.71 |

| 0.00417 |

$4473.09 |

$5.35 |

| 0.004167 |

$4468.28 |

$0.54 |

| 0.0041667 |

$4467.80 |

$0.06 |

| no rounding |

$4467.74 |

|

If you’re working in a bank, of course you wouldn’t round at all. For our purposes, the answer we got by rounding to 0.00417, three significant digits, is close enough—$5 off of $4500 isn’t too bad. Certainly keeping that fourth decimal place wouldn’t have hurt.

Using Your Calculator

In many cases, you can avoid rounding completely by how you enter things in your calculator. For example, in the example above, we needed to calculate

[latex-display]\displaystyle\\P_{30}=1000\left(1+\frac{0.05}{12}\right)^{12\cdot{30}}[/latex-display]

We can quickly calculate 12 × 30 = 360, giving [latex]\displaystyle\\P_{30}=1000\left(1+\frac{0.05}{12}\right)^{360}[/latex].

Now we can use the calculator.

| Type This |

Calculator Shows |

|---|

| 0.05 ÷ 12 = |

0.00416666666667 |

| + 1 = |

1.00416666666667 |

| yx 360 = |

4.46774431400613 |

| × 1000 = |

4467.74431400613 |

Using Your Calculator Continued

The previous steps were assuming you have a “one operation at a time” calculator; a more advanced calculator will often allow you to type in the entire expression to be evaluated. If you have a calculator like this, you will probably just need to enter:

1000 × (1 + 0.05 ÷ 12) yx 360 = .

Annuities

For most of us, we aren’t able to put a large sum of money in the bank today. Instead, we save for the future by depositing a smaller amount of money from each paycheck into the bank. This idea is called a savings annuity. Most retirement plans like 401k plans or IRA plans are examples of savings annuities.

An annuity can be described recursively in a fairly simple way. Recall that basic compound interest follows from the relationship

[latex-display]\displaystyle{P}_m=\left(1+\frac{r}{k}\right)P_{m-1}\\[/latex-display]

For a savings annuity, we simply need to add a deposit, d, to the account with each compounding period:

[latex-display]\displaystyle{P}_m=\left(1+\frac{r}{k}\right)P_{m-1}+d\\[/latex-display]

Taking this equation from recursive form to explicit form is a bit trickier than with compound interest. It will be easiest to see by working with an example rather than working in general.

Suppose we will deposit $100 each month into an account paying 6% interest. We assume that the account is compounded with the same frequency as we make deposits unless stated otherwise. In this example:

- r = 0.06 (6%)

- k = 12 (12 compounds/deposits per year)

- d = $100 (our deposit per month)

Writing out the recursive equation gives

[latex-display]\displaystyle{P}_m=\left(1+\frac{0.06}{12}\right)P_{m-1}+100=(1.005)P_{m-1}+100\\[/latex-display]

Assuming we start with an empty account, we can begin using this relationship:

[latex-display]P_0=0\\[/latex-display]

[latex-display]P_1=(1.005)P_0+100=100\\[/latex-display]

[latex-display]P_2=(1.005)P_1+100=(1.005)100+100=100(1.005)+100\\[/latex-display]

[latex-display]P_3=(1.005)P_2+100=(1.005)(100(1.005)+100)+100=100(1.005)^2+100(1.005)+100\\[/latex-display]

Continuing this pattern, after m deposits, we’d have saved:

[latex-display]{P_m}=100(1.005)^{m-1}+100(1.005)^{m-2}+\cdot\cdot\cdot{+}100(1.005)+100\\[/latex-display]

In other words, after m months, the first deposit will have earned compound interest for m − 1 months. The second deposit will have earned interest for m − 2 months. Last months deposit would have earned only one month worth of interest. The most recent deposit will have earned no interest yet.

This equation leaves a lot to be desired, though—it doesn’t make calculating the ending balance any easier! To simplify things, multiply both sides of the equation by 1.005:

[latex-display]1.005{P}_m=1.005\left(100(1.005)^{m-1}+100(1.005)^{m-2}+100(1.005)+\cdot\cdot\cdot{+}100(1.005)+100\right)\\[/latex-display]

Distributing on the right side of the equation gives

[latex-display]1.005{P}_m=100(1.005)^m+100(1.005)^{m-1}+\cdot\cdot\cdot{+}100(1.005)^2+100(1.005)\\[/latex-display]

Now we’ll line this up with like terms from our original equation, and subtract each side

[latex-display]1.005{P}_m=100(1.005)^m+100(1.005)^{m-1}+\cdot\cdot\cdot{+}100(1.005)\\[/latex-display]

[latex-display]P_m=100(1.005)^{m-1}+\cdot\cdot\cdot{+}100(1.005)+100\\[/latex-display]

Almost all the terms cancel on the right hand side when we subtract, leaving

[latex-display]1.005{P}_m-P_m=100(1.005)^m-100\\[/latex-display]

Solving for Pm

[latex-display]0.005P_m=100{\big(}(1.005)^m-1{\big)}\\[/latex-display]

[latex-display]\displaystyle{P_m}=\frac{100{\big(}(1.005)^m-1{\big)}}{0.005}\\[/latex-display]

Replacing m months with 12N, where N is measured in years, gives

[latex-display]\displaystyle{P_N}=\frac{100{\big(}(1.005)^{12N}-1{\big)}}{0.005}\\[/latex-display]

Recall 0.005 was [latex]\displaystyle\frac{r}{k}\\[/latex] and 100 was the deposit d. 12 was k, the number of deposit each year. Generalizing this result, we get the saving annuity formula.

Annuity Formula

[latex-display]\displaystyle{P}_N=\frac{d\left(\left(1+\frac{r}{k}\right)^{Nk}-1\right)}{\left(\frac{r}{k}\right)}\\[/latex-display]

- PN is the balance in the account after N years.

- d is the regular deposit (the amount you deposit each year, each month, etc.)

- r is the annual interest rate in decimal form.

- k is the number of compounding periods in one year.

If the compounding frequency is not explicitly stated, assume there are the same number of compounds in a year as there are deposits made in a year.

For example, if the compounding frequency isn’t stated:

If you make your deposits every month, use monthly compounding, k = 12.

If you make your deposits every year, use yearly compounding, k = 1.

If you make your deposits every quarter, use quarterly compounding, k = 4.

Etc.

When Do You Use This?

Annuities assume that you put money in the account on a regular schedule (every month, year, quarter, etc.) and let it sit there earning interest.

Compound interest assumes that you put money in the account once and let it sit there earning interest.

Compound interest: One deposit

Annuity: Many deposits.

Example 7

A traditional individual retirement account (IRA) is a special type of retirement account in which the money you invest is exempt from income taxes until you withdraw it. If you deposit $100 each month into an IRA earning 6% interest, how much will you have in the account after 20 years?

Solution

In this example,

| d = $100 |

the monthly deposit |

| r = 0.06 |

6% annual rate |

| k = 12 |

since we’re doing monthly deposits, we’ll compound monthly |

| N = 20 |

we want the amount after 20 years |

Putting this into the equation:

[latex-display]\displaystyle{P}_{20}=\frac{100\left(\left(1+\frac{0.06}{12}\right)^{20(12)}-1\right)}{\left(\frac{0.06}{12}\right)}\\[/latex-display]

[latex-display]\displaystyle{P}_{20}=\frac{100\left(\left(1.005\right)^{240}-1\right)}{\left({0.005}\right)}\\[/latex-display]

[latex-display]\displaystyle{P}_{20}=\frac{100\left(3.310-1\right)}{\left({0.005}\right)}\\[/latex-display]

[latex-display]\displaystyle{P}_{20}=\frac{100\left(2.310\right)}{\left({0.005}\right)}=\$46200\\[/latex-display]

The account will grow to $46,200 after 20 years.

Notice that you deposited into the account a total of $24,000 ($100 a month for 240 months). The difference between what you end up with and how much you put in is the interest earned. In this case it is $46,200 − $24,000 = $22,200.

Example 8

You want to have $200,000 in your account when you retire in 30 years. Your retirement account earns 8% interest. How much do you need to deposit each month to meet your retirement goal?

Solution

In this example, we’re looking for

d.

| r = 0.08 |

8% annual rate |

| k = 12 |

since we’re depositing monthly |

| N = 30 |

30 years |

| P30 = $200,000 |

The amount we want to have in 30 years |

In this case, we’re going to have to set up the equation, and solve for

d.

[latex-display]\displaystyle{200,000}=\frac{d\left(\left(1+\frac{0.08}{12}\right)^{30(12)}-1\right)}{\left(\frac{0.08}{12}\right)}\\[/latex-display]

[latex-display]\displaystyle{200,000}=\frac{d\left(\left(1.00667\right)^{360}-1\right)}{\left(0.00667\right)}\\[/latex-display]

[latex-display]\displaystyle{200,000}=d\left(1491.57\right)\\[/latex-display]

[latex-display]\displaystyle{d}=\frac{200,000}{1491.57}=\$134.09\\[/latex-display]

So you would need to deposit $134.09 each month to have $200,000 in 30 years if your account earns 8% interest

Try It Now

A more conservative investment account pays 3% interest. If you deposit $5 a day into this account, how much will you have after 10 years? How much is from interest?

Payout Annuities

In the last section you learned about annuities. In an annuity, you start with nothing, put money into an account on a regular basis, and end up with money in your account.

In this section, we will learn about a variation called a Payout Annuity. With a payout annuity, you start with money in the account, and pull money out of the account on a regular basis. Any remaining money in the account earns interest. After a fixed amount of time, the account will end up empty.

Payout annuities are typically used after retirement. Perhaps you have saved $500,000 for retirement, and want to take money out of the account each month to live on. You want the money to last you 20 years. This is a payout annuity. The formula is derived in a similar way as we did for savings annuities. The details are omitted here.

Payout Annuity Formula

[latex-display]\displaystyle{P}_0=\frac{d\left({1}-\left(1+\frac{r}{k}\right)^{-Nk}\right)}{\left(\frac{r}{k}\right)}\\[/latex-display]

- P0 is the balance in the account at the beginning (starting amount, or principal).

- d is the regular withdrawal (the amount you take out each year, each month, etc.)

- r is the annual interest rate (in decimal form. Example: 5% = 0.05)

- k is the number of compounding periods in one year.

- N is the number of years we plan to take withdrawals

Like with annuities, the compounding frequency is not always explicitly given, but is determined by how often you take the withdrawals.

When Do You Use This

Payout annuities assume that you

take money from the account

on a regular schedule (

every month, year, quarter, etc.) and let the rest sit there earning interest.

- Compound interest: One deposit

- Annuity: Many deposits.

- Payout Annuity: Many withdrawals

Example 9

After retiring, you want to be able to take $1000 every month for a total of 20 years from your retirement account. The account earns 6% interest. How much will you need in your account when you retire?

Solution

In this example,

| d = $1000 |

the monthly withdrawal |

| r = 0.06 |

6% annual rate |

| k = 12 |

since we’re doing monthly withdrawals, we’ll compound monthly |

| N = 20 |

since were taking withdrawals for 20 years |

We’re looking for

P0; how much money needs to be in the account at the beginning.

Putting this into the equation:

[latex-display]\displaystyle{P}_{0}=\frac{1000\left(1-\left(1+\frac{0.06}{12}\right)^{-20(12)}\right)}{\left(\frac{0.06}{12}\right)}\\[/latex-display]

[latex-display]\displaystyle{P}_{0}=\frac{1000\left(1-\left(1.005\right)^{-240}\right)}{\left(0.005\right)}\\[/latex-display]

[latex-display]\displaystyle{P}_{0}=\frac{1000\left(1-0.302\right)}{\left(0.005\right)}=\$139,600\\[/latex-display]

You will need to have $139,600 in your account when you retire.

Notice that you withdrew a total of $240,000 ($1000 a month for 240 months). The difference between what you pulled out and what you started with is the

interest earned. In this case it is $240,000 − $139,600 = $100,400 in interest.

Evaluating Negative Exponents on Your Calculator

With these problems, you need to raise numbers to negative powers. Most calculators have a separate button for negating a number that is different than the subtraction button. Some calculators label this (-), some with +/-. The button is often near the = key or the decimal point.

If your calculator displays operations on it (typically a calculator with multiline display), to calculate 1.005−240 you'd type something like: 1.005 ^ (-) 240

If your calculator only shows one value at a time, then usually you hit the (-) key after a number to negate it, so you'd hit: 1.005 yx 240 (-) =

Give it a try—you should get 1.005−240 = 0.302096

Example 10

You know you will have $500,000 in your account when you retire. You want to be able to take monthly withdrawals from the account for a total of 30 years. Your retirement account earns 8% interest. How much will you be able to withdraw each month?

Solution

In this example, we’re looking for

d.

| r = 0.08 |

8% annual rate |

| k = 12 |

since we’re withdrawing monthly |

| N = 30 |

30 years |

| P0 = $500,000 |

we are beginning with $500,000 |

In this case, we’re going to have to set up the equation, and solve for

d.

[latex-display]\displaystyle{500,000}=\frac{d\left(1-\left(1+\frac{0.08}{12}\right)^{-30(12)}\right)}{\left(\frac{0.08}{12}\right)}\\[/latex-display]

[latex-display]\displaystyle{500,000}=\frac{d\left(1-\left(1.00667\right)^{-360}\right)}{\left(0.00667\right)}\\[/latex-display]

[latex-display]\displaystyle{500,000}=d\left({136.232}\right)\\[/latex-display]

[latex-display]\displaystyle{d}=\frac{500,000}{136.232}=\$3670.21\\[/latex-display]

You would be able to withdraw $3,670.21 each month for 30 years.

Try It Now

A donor gives $100,000 to a university, and specifies that it is to be used to give annual scholarships for the next 20 years. If the university can earn 4% interest, how much can they give in scholarships each year?

Loans

In the last section, you learned about payout annuities.

In this section, you will learn about conventional loans (also called amortized loans or installment loans). Examples include auto loans and home mortgages. These techniques do not apply to payday loans, add-on loans, or other loan types where the interest is calculated up front.

One great thing about loans is that they use exactly the same formula as a payout annuity. To see why, imagine that you had $10,000 invested at a bank, and started taking out payments while earning interest as part of a payout annuity, and after 5 years your balance was zero. Flip that around, and imagine that you are acting as the bank, and a car lender is acting as you. The car lender invests $10,000 in you. Since you’re acting as the bank, you pay interest. The car lender takes payments until the balance is zero.

Loans Formula

[latex-display]\displaystyle{P}_0=\frac{d\left({1}-\left(1+\frac{r}{k}\right)^{-Nk}\right)}{\left(\frac{r}{k}\right)}\\[/latex-display]

- P0 is the balance in the account at the beginning (the principal, or amount of the loan).

- d is your loan payment (your monthly payment, annual payment, etc)

- r is the annual interest rate in decimal form.

- k is the number of compounding periods in one year.

- N is the length of the loan, in years

Like before, the compounding frequency is not always explicitly given, but is determined by how often you make payments.

When do you use this

The loan formula assumes that you make loan payments

on a regular schedule (

every month, year, quarter, etc.) and are paying interest on the loan.

- Compound interest: One deposit

- Annuity: Many deposits.

- Payout Annuity: Many withdrawals

- Loans: Many payments

Example 11

You can afford $200 per month as a car payment. If you can get an auto loan at 3% interest for 60 months (5 years), how expensive of a car can you afford? In other words, what amount loan can you pay off with $200 per month?

Solution

In this example,

| d = $200 |

the monthly loan payment |

| r = 0.03 |

3% annual rate |

| k = 12 |

since we’re doing monthly payments, we’ll compound monthly |

| N = 5 |

since we’re making monthly payments for 5 years |

We’re looking for

P0, the starting amount of the loan.

[latex-display]\displaystyle{P}_{0}=\frac{200\left(1-\left(1+\frac{0.03}{12}\right)^{-5(12)}\right)}{\left(\frac{0.03}{12}\right)}\\[/latex-display]

[latex-display]\displaystyle{P}_{0}=\frac{200\left(1-\left(1.0025\right)^{-60}\right)}{\left(0.0025\right)}\\[/latex-display]

[latex-display]\displaystyle{P}_{0}=\frac{200\left(1-0.861\right)}{\left(0.0025\right)}=\$11,120\\[/latex-display]

You can afford a $11,120 loan.

You will pay a total of $12,000 ($200 per month for 60 months) to the loan company. The difference between the amount you pay and the amount of the loan is the

interest paid. In this case, you’re paying $12,000 − $11,120 = $880 interest total.

Example 12

You want to take out a $140,000 mortgage (home loan). The interest rate on the loan is 6%, and the loan is for 30 years. How much will your monthly payments be?

Solution

In this example, we’re looking for

d.

| r = 0.06 |

6% annual rate |

| k = 12 |

since we’re paying monthly |

| N = 30 |

30 years |

| P0 = $140,000 |

the starting loan amount |

In this case, we’re going to have to set up the equation, and solve for

d.

[latex-display]\displaystyle{140,000}=\frac{d\left(1-\left(1+\frac{0.06}{12}\right)^{-30(12)}\right)}{\left(\frac{0.06}{12}\right)}\\[/latex-display]

[latex-display]\displaystyle{140,000}=\frac{d\left(1-\left(1.005\right)^{-360}\right)}{\left(0.005\right)}\\[/latex-display]

[latex-display]\displaystyle{140,000}=d\left({166.792}\right)\\[/latex-display]

[latex-display]\displaystyle{d}=\frac{140,000}{166.792}=\$839.37\\[/latex-display]

You will make payments of $839.37 per month for 30 years.

You’re paying a total of $302,173.20 to the loan company: $839.37 per month for 360 months. You are paying a total of $302,173.20 − $140,000 = $162,173.20 in interest over the life of the loan.

Try It Now

Janine bought $3,000 of new furniture on credit. Because her credit score isn’t very good, the store is charging her a fairly high interest rate on the loan: 16%. If she agreed to pay off the furniture over 2 years, how much will she have to pay each month?

Remaining Loan Balance

With loans, it is often desirable to determine what the remaining loan balance will be after some number of years. For example, if you purchase a home and plan to sell it in five years, you might want to know how much of the loan balance you will have paid off and how much you have to pay from the sale.

To determine the remaining loan balance after some number of years, we first need to know the loan payments, if we don’t already know them. Remember that only a portion of your loan payments go towards the loan balance; a portion is going to go towards interest. For example, if your payments were $1,000 a month, after a year you will not have paid off $12,000 of the loan balance.

To determine the remaining loan balance, we can think “how much loan will these loan payments be able to pay off in the remaining time on the loan?”

Example 13

If a mortgage at a 6% interest rate has payments of $1,000 a month, how much will the loan balance be 10 years from the end the loan?

Solution

To determine this, we are looking for the amount of the loan that can be paid off by $1,000 a month payments in 10 years. In other words, we’re looking for

P0 when

| d = $1,000 |

the monthly loan payment |

| r = 0.06 |

6% annual rate |

| k = 12 |

since we’re doing monthly payments, we’ll compound monthly |

| N = 10 |

since we’re making monthly payments for 10 more years |

[latex-display]\displaystyle{P}_{0}=\frac{1000\left(1-\left(1+\frac{0.06}{12}\right)^{-10(12)}\right)}{\left(\frac{0.06}{12}\right)}\\[/latex-display]

[latex-display]\displaystyle{P}_{0}=\frac{1000\left(1-\left(1.005\right)^{-120}\right)}{\left(0.005\right)}\\[/latex-display]

[latex-display]\displaystyle{P}_{0}=\frac{200\left(1-0.5496\right)}{\left(0.005\right)}=\$90,073.45\\[/latex-display]

The loan balance with 10 years remaining on the loan will be $90,073.45

Often times answering remaining balance questions requires two steps:

- Calculating the monthly payments on the loan

- Calculating the remaining loan balance based on the remaining time on the loan

Example 14

A couple purchases a home with a $180,000 mortgage at 4% for 30 years with monthly payments. What will the remaining balance on their mortgage be after 5 years?

Solution

First we will calculate their monthly payments. We’re looking for

d.

| r = 0.04 |

4% annual rate |

| k = 12 |

since they’re paying monthly |

| N = 30 |

30 years |

| P0 = $180,000 |

the starting loan amount |

We set up the equation and solve for

d.

[latex-display]\displaystyle{180,000}=\frac{d\left(1-\left(1+\frac{0.04}{12}\right)^{-30(12)}\right)}{\left(\frac{0.04}{12}\right)}\\[/latex-display]

[latex-display]\displaystyle{180,000}=\frac{d\left(1-\left(1.00333\right)^{-360}\right)}{\left(.00333\right)}\\[/latex-display]

[latex-display]\displaystyle{180,000}=d\left({209.562}\right)\\[/latex-display]

[latex-display]\displaystyle{d}=\frac{180,000}{209.562}=\$858.93\\[/latex-display]

Now that we know the monthly payments, we can determine the remaining balance. We want the remaining balance after 5 years, when 25 years will be remaining on the loan, so we calculate the loan balance that will be paid off with the monthly payments over those 25 years.

| d = $858.93 |

the monthly loan payment we calculated above |

| r = 0.04 |

4% annual rate |

| k = 12 |

since they’re doing monthly payments |

| N = 25 |

since they’d be making monthly payments for 25 more years |

[latex-display]\displaystyle{P}_{0}=\frac{858.93\left(1-\left(1+\frac{0.04}{12}\right)^{-25(12)}\right)}{\left(\frac{0.04}{12}\right)}\\[/latex-display]

[latex-display]\displaystyle{P}_{0}=\frac{858.93\left(1-\left(1.00333\right)^{-300}\right)}{\left(0.00333\right)}\\[/latex-display]

[latex-display]\displaystyle{P}_{0}=\frac{858.93\left(1-0.369\right)}{\left(0.00333\right)}=\$162,758.26\\[/latex-display]

The loan balance after 5 years, with 25 years remaining on the loan, will be $162,758.26.

Over that 5 years, the couple has paid off $180,000 − $162.758.26 = $17,241.74 of the loan balance. They have paid a total of $858.93 a month for 5 years (60 months), for a total of $51,535.80, so $51,535.80 − $17,241.74 = $34,294.06 of what they have paid so far has been interest.

Which Equation to Use?

When presented with a finance problem (on an exam or in real life), you're usually not told what type of problem it is or which equation to use. Here are some hints on deciding which equation to use based on the wording of the problem.

The easiest types of problem to identify are loans. Loan problems almost always include words like: "loan," "amortize" (the fancy word for loans), "finance (a car)," or "mortgage" (a home loan). Look for these words. If they're there, you're probably looking at a loan problem. To make sure, see if you're given what your monthly (or annual) payment is, or if you're trying to find a monthly payment.

If the problem is not a loan, the next question you want to ask is: "Am I putting money in an account and letting it sit, or am I making regular (monthly/annually/quarterly) payments or withdrawals?" If you're letting the money sit in the account with nothing but interest changing the balance, then you're looking at a compound interest problem. The exception would be bonds and other investments where the interest is not reinvested; in those cases you’re looking at simple interest.

If you're making regular payments or withdrawals, the next questions is: "Am I putting money into the account, or am I pulling money out?" If you're putting money into the account on a regular basis (monthly/annually/quarterly) then you're looking at a basic Annuity problem. Basic annuities are when you are saving money. Usually in an annuity problem, your account starts empty, and has money in the future.

If you're pulling money out of the account on a regular basis, then you're looking at a Payout Annuity problem. Payout annuities are used for things like retirement income, where you start with money in your account, pull money out on a regular basis, and your account ends up empty in the future.

Remember, the most important part of answering any kind of question, money or otherwise, is first to correctly identify what the question is really asking, and to determine what approach will best allow you to solve the problem.

Try It Now

For each of the following scenarios, determine if it is a compound interest problem, a savings annuity problem, a payout annuity problem, or a loans problem. Then solve each problem.

- Marcy received an inheritance of $20,000, and invested it at 6% interest. She is going to use it for college, withdrawing money for tuition and expenses each quarter. How much can she take out each quarter if she has 3 years of school left?

- Paul wants to buy a new car. Rather than take out a loan, he decides to save $200 a month in an account earning 3% interest compounded monthly. How much will he have saved up after 3 years?

- Keisha is managing investments for a non-profit company. They want to invest some money in an account earning 5% interest compounded annually with the goal to have $30,000 in the account in 6 years. How much should Keisha deposit into the account?

- Miao is going to finance new office equipment at a 2% rate over a 4 year term. If she can afford monthly payments of $100, how much new equipment can she buy?

- How much would you need to save every month in an account earning 4% interest to have $5,000 saved up in two years?

Solving for Time

Often we are interested in how long it will take to accumulate money or how long we’d need to extend a loan to bring payments down to a reasonable level.

Note: This section assumes you’ve covered solving exponential equations using logarithms, either in prior classes or in the growth models chapter.

Example 15

If you invest $2000 at 6% compounded monthly, how long will it take the account to double in value?

Solution

This is a compound interest problem, since we are depositing money once and allowing it to grow. In this problem,

| P0 = $2000 |

the initial deposit |

| r = 0.06 |

6% annual rate |

| k = 12 |

12 months in 1 year |

So our general equation is:

[latex-display]\displaystyle{P_N}={2000}\left(1+\frac{0.06}{12}\right)^{N\cdot12}\\[/latex-display]

We also know that we want our ending amount to be double of $2000, which is $4000, so we’re looking for

N so that

PN = 4000. To solve this, we set our equation for

PN equal to 4000.

| [latex]\displaystyle{4000}={2000}\left(1+\frac{0.06}{12}\right)^{N\cdot{12}}\\[/latex] |

Divide both sides by 2000 |

| [latex]2=(1.005)^{12N}\\[/latex] |

To solve for the exponent, take the log of both sides |

| [latex]\log(2)=\log\left(\left(1.005\right)^{12N}\right)\\[/latex] |

Use the exponent property of logs on the right side |

| [latex]\log(2)=12N\log(1.005)\\[/latex] |

Now we can divide both sides by 12log(1.005) |

| [latex]\displaystyle\frac{\log(2)}{12\log(1.005)}=N\\[/latex] |

Approximating this to a decimal |

| N = 11.581 |

|

It will take about 11.581 years for the account to double in value. Note that your answer may come out slightly differently if you had evaluated the logs to decimals and rounded during your calculations, but your answer should be close. For example if you rounded log(2) to 0.301 and log(1.005) to 0.00217, then your final answer would have been about 11.577 years.

Example 16

If you invest $100 each month into an account earning 3% compounded monthly, how long will it take the account to grow to $10,000?

Solution

This is a savings annuity problem since we are making regular deposits into the account.

| d = $100 |

the monthly deposit |

| r = 0.03 |

3% annual rate |

| k = 12 |

since we’re doing monthly deposits, we’ll compound monthly |

We don’t know

N, but we want

PN to be $10,000.

Putting this into the equation:

[latex-display]\displaystyle{10,000}=\frac{100\left(\left(1+\frac{0.03}{12}\right)^{N(12)}-1\right)}{\left(\frac{0.03}{12}\right)}\\[/latex-display]

Simplifying the fractions a bit

[latex-display]\displaystyle{10,000}=\frac{100\left(\left({1.0025}\right)^{12N}-1\right)}{0.0025}\\[/latex-display]

We want to isolate the exponential term, 1.0025

12N, so multiply both sides by 0.0025

| [latex]25=100\left(\left(1.0025\right)^{12N}-1\right)\\[/latex] |

Divide both sides by 100 |

| [latex]0.25=\left(1.0025\right)^{12N}-1\\[/latex] |

Add 1 to both sides |

| [latex]1.25=\left(1.0025\right)^{12N}\\[/latex] |

Now take the log of both sides |

| [latex]\log\left(1.25\right)=\log\left(\left(1.0025\right)^{12N}\right)\\[/latex] |

Use the exponent property of logs |

| [latex]\log\left(1.25\right)=12N\log(1.0025)\\[/latex] |

Divide by 12log(1.0025) |

| [latex]\displaystyle\frac{\log(1.25)}{12\log(1.0025)}=N\\[/latex] |

Approximating to a decimal |

| N = 7.447 years |

|

It will take about 7.447 years to grow the account to $10,000.

Try It Now

Joel is considering putting a $1,000 laptop purchase on his credit card, which has an interest rate of 12% compounded monthly. How long will it take him to pay off the purchase if he makes payments of $30 a month?

Licenses & Attributions

CC licensed content, Shared previously